Finance

7 Ways AI Investment Banks Are Reshaping Back-Office Finance

See how the AI investment bank is eliminating late-night manual work and costly errors across settlements, compliance, and reconciliation. Real results inside.

Sanya Shah

Co-founder, Predflow

At 11:45 PM, a team of three operations staff is manually matching trade confirmations against internal records before the settlement window closes. One mismatch in a thousand-line spreadsheet will hold up the entire batch. This is not a story from 2010. It is happening in bank back offices right now.

Investment banks are not hiring their way out of this problem. Headcount costs too much, scales too slowly, and does not solve the underlying issue: processes built on manual handoffs between systems that cannot talk to each other. The shift accelerating through 2025 and 2026 is AI investment bank deployments moving out of front-office chatbots and into deep back-office workflow automation. AI adoption among investment managers is surging, and the most significant changes are happening in operations, not on trading desks.

This article breaks down exactly seven back-office functions where AI is being deployed today, what it replaces, and what it means for operations leaders still relying on manual handoffs and fragmented tools.

Why AI Investment Banks Are Starting in the Back Office, Not the Front

The hidden cost center most banks are finally measuring

Back-office operations in investment banking consume a disproportionate share of total operating costs. Reconciliation teams, compliance staff, and reporting analysts spend most of their time on work that is repetitive, rule-based, and error-prone at scale. These teams rarely appear in transformation roadmaps, but they represent the largest concentration of manual labor in the institution.

Operations leaders are now measuring this cost directly. When you calculate fully loaded headcount costs, error correction cycles, and the regulatory risk of missed deadlines, the back office stops looking like overhead and starts looking like the highest-priority automation target in the building.

Why front-office AI tools stalled while back-office automation scaled

Front-office AI tools, primarily client-facing chatbots and trading analytics, ran into two problems: regulatory scrutiny on client interactions and the difficulty of building AI that handles nuanced, high-stakes decisions reliably. Back-office processes are different. They are structured, rule-bound, and high-volume. That makes them well-suited to AI automation in a way that front-office judgment calls are not.

Artificial intelligence in investment banking is finding its fastest adoption where the work is most clearly defined and the cost of errors is measurable. That means operations, compliance, and reporting functions are moving first. Banking risk and management frameworks that once slowed front-office AI adoption are actually accelerating back-office deployments because the governance requirements are cleaner.

1. Automated Trade Reconciliation: Eliminating the Overnight Manual Queue

What the manual process actually costs per reconciliation cycle

A mid-size investment bank processing several thousand trades per day runs a reconciliation cycle that requires staff to match confirmations from counterparties against internal booking systems, flag mismatches, and resolve breaks before settlement deadlines. Manual reconciliation at that volume produces error rates that compound: one missed break creates downstream settlement failures, regulatory reporting gaps, and operational risk events.

The fully loaded cost includes overnight staffing, error correction time, and the occasional settlement failure penalty. None of those costs appear on a single line in the budget, which is why they persist.

How AI agents handle mismatches and route exceptions with context

AI agents in reconciliation do not simply automate the matching step. They apply business rules and context to decide what a mismatch means. A one-cent discrepancy on a $10 million trade gets treated differently than a full confirmation missing from a counterparty. The agent routes each exception to the right team with the relevant context already attached, instead of dumping every break into a queue for a human to triage from scratch.

Artificial intelligence in trading processes has demonstrated the ability to handle the high-volume, rules-based matching work at any hour. Human teams focus on genuine exceptions that require judgment. The overnight queue shrinks from hundreds of items to a handful of real breaks, with real-time monitoring providing a live status view rather than a morning report.

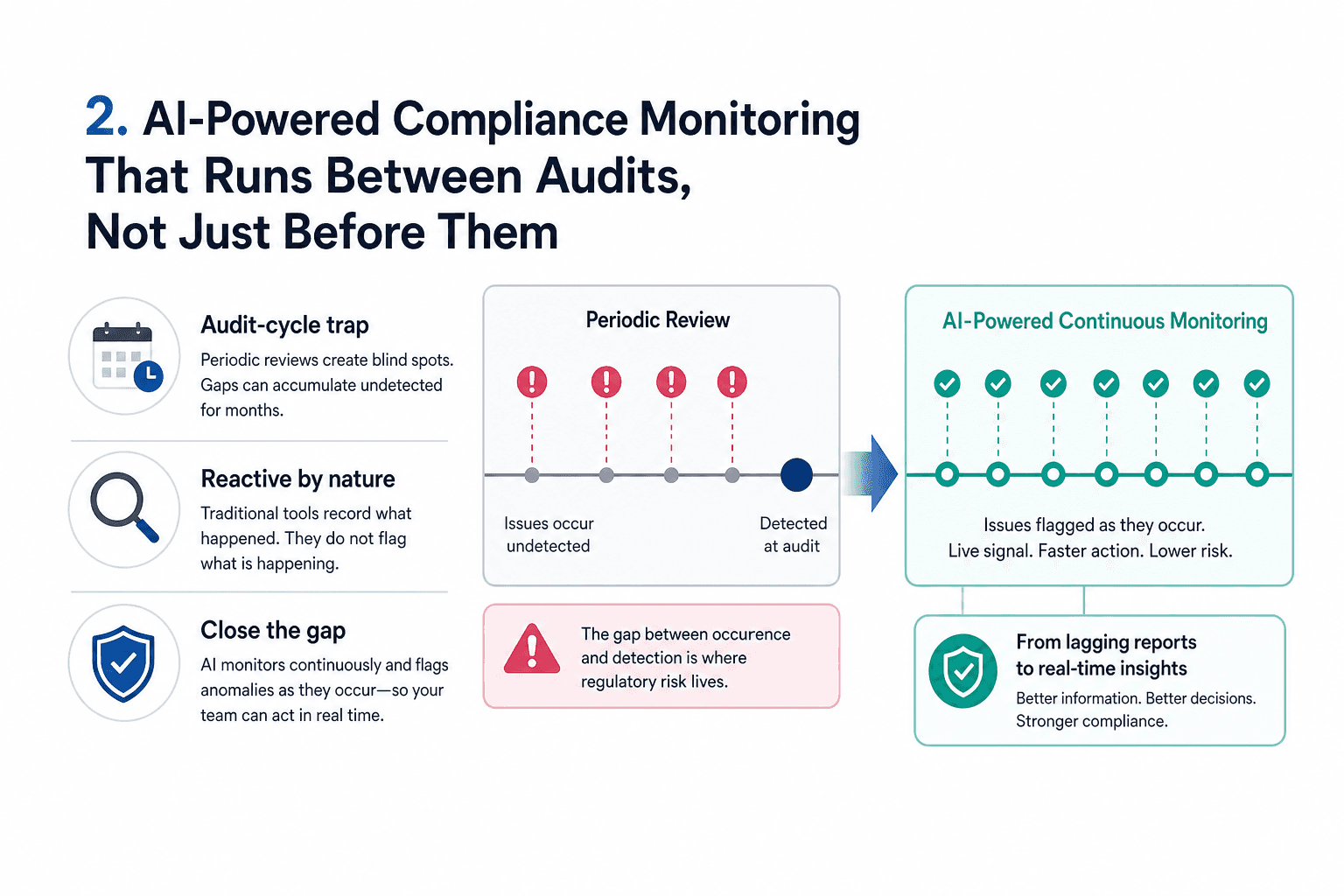

2. AI-Powered Compliance Monitoring That Runs Between Audits, Not Just Before Them

The audit-cycle trap and why it creates regulatory blind spots

Most back-office compliance processes operate on a periodic review cycle: documentation is assembled, controls are tested, and gaps are identified in the weeks before an audit. Between cycles, compliance gaps can accumulate undetected for months. The audit-cycle trap means that the compliance picture a bank presents to regulators reflects a snapshot, not ongoing operational reality.

Auditing software tools and siem monitoring tools have historically been reactive. They record what happened. They do not flag what is happening. The gap between occurrence and detection is where regulatory risk lives.

Continuous monitoring versus periodic review: what changes operationally

AI-powered compliance monitoring changes the operational model by running checks continuously against transaction data, communication records, and process logs. Anomalies are flagged as they occur, not when a reviewer gets to them. The operations team receives a live signal rather than a lagging report.

It is important to be direct about one limitation here. Continuous monitoring surfaces more exceptions than periodic review. That is by design, but it means the volume of items requiring human review increases initially. The risk of artificial intelligence tools in compliance is that teams interpret more alerts as more work rather than better information. Good implementation filters alerts by severity and routes them to the right reviewer, so the signal is actionable rather than overwhelming. AI augments the compliance team. It does not remove the human checkpoint that regulations require.

3. Invoice and Accounts Payable Automation Across Multi-Entity Bank Structures

Where manual invoice processing breaks down in multi-entity structures

An investment bank operating across multiple legal entities processes invoices that arrive in different currencies, reference different cost centers, and require approval chains that vary by entity and spend threshold. Manual processing means someone is copying data between systems, chasing approvals by email, and checking for duplicate vendor entries by hand. Three-way matching, where the purchase order, goods receipt, and invoice are reconciled against each other, frequently fails not because the data is wrong but because it is in three different systems with no automated bridge.

Billing system software and accounts payable and receivable software designed for single-entity businesses do not handle this complexity natively. The result is a backlog that grows with transaction volume.

What AI-handled invoice routing looks like end to end

AI agents built for invoice processing can extract data from incoming invoices regardless of format, run PO matching against the procurement system, check for duplicate vendor entries across entities, apply the correct approval routing logic based on entity, currency, and amount, and flag discrepancies before any payment is triggered. The agent owns the entire workflow from receipt to approval readiness. Human sign-off is required only at defined thresholds, not at every step.

Platforms like Predflow take a process-mapping-first approach, meaning the agent understands the full invoice lifecycle, including the exceptions, before automation begins. Edge cases like currency mismatches, missing PO references, and duplicate vendor records are handled by the agent rather than escalated to a human by default. That distinction matters because most invoice automation failures happen at the edges, not in the standard flow.

4. AI Investment Bank Use Case: Intelligent Regulatory Reporting Without Manual Data Pulls

Why regulatory reporting consumes disproportionate analyst hours

Regulatory reporting requirements under frameworks like MiFID II, Basel III disclosures, and EMIR generate significant reporting obligations that require pulling data from multiple source systems, formatting it to specific regulatory templates, and submitting within defined windows. A reporting team at a mid-size investment bank can spend the majority of its cycle time on data aggregation, not on analysis or verification. The actual intelligence work, checking that the report reflects operational reality, happens in whatever time remains.

This is a structural problem. The analysts doing the aggregation are overqualified for it. The enterprise software solutions they work in were not designed to produce regulatory outputs natively.

From data aggregation to submission-ready output: what AI handles

An AI investment bank deployment in regulatory reporting connects to the relevant source systems, aggregates the required data fields according to the reporting template, identifies inconsistencies between data sources before they appear in a submission, and produces a review-ready report. The human team reviews and approves the output. They do not build it from scratch.

Automated performance monitoring can also track whether source data is arriving on schedule and flag delays before they affect the submission window. The shift is from analysts spending 80% of their time gathering data to spending that time verifying and submitting it. That is the practical difference between report generation automation and regulatory intelligence.

5. AI-Driven Vendor and Software License Management Across Fragmented Tool Stacks

The hidden cost of fragmented software procurement in banking

Investment bank back offices accumulate software tools over years of individual team purchases. A typical operations environment includes multiple data providers with overlapping coverage, redundant analytics platforms bought by different desks, legacy risk tools that predate current platforms, and monitoring tools added during specific compliance projects. Software license management across this environment is rarely centralized.

The result is predictable: licenses are renewed automatically because no one has visibility into usage, tools with duplicate functionality are paid for by different cost centers, and renewal windows pass without negotiation because no one tracked them. Software licensing compliance becomes a reactive exercise when audits surface gaps.

What AI-assisted software asset management actually tracks

AI-assisted software asset management builds a live inventory of tools, users, usage frequency, contract terms, and renewal dates. It surfaces underused licenses before renewal, identifies overlapping tools across teams, and flags compliance gaps where software is in use without a current license. IT asset management software has historically required manual data collection to build this picture. AI agents can maintain it continuously by pulling from procurement systems, access logs, and contract repositories.

For operations leaders, the governance benefit is that tool sprawl does not recur. The system flags new tool requests against existing capabilities, preventing duplicate purchases before they happen.

6. Straight-Through Processing for Client Onboarding: Cutting Days to Hours

Where onboarding queues pile up and why manual review is not the bottleneck you think it is

Institutional client onboarding at investment banks takes between 30 and 90 days in standard practice. Most operations leaders identify the KYC review as the bottleneck. The actual bottleneck is usually earlier: document collection, data entry into the client management system, and the multiple handoffs between teams before any human review even begins. By the time a compliance officer sees the file, it has already spent two weeks moving between inboxes.

Customer management software and business system software store the data once it arrives, but they do not move it through the process. That movement is still manual.

Straight-through processing rates: what leading banks are achieving

AI co-pilots are already easing painful tasks for bank staff, including investment bankers handling onboarding workflows. Straight-through processing in client onboarding means the AI agent collects documents, validates completeness, populates the client record, runs initial screening checks, and routes the file for human review only when a genuine decision point is reached.

Leading implementations are compressing onboarding timelines significantly for clients who arrive with clean documentation. The human review step for sanctions screening and final KYC sign-off remains in place. Regulations require it and that is appropriate. What changes is that the human reviewer receives a complete, verified file rather than a partially assembled one. That is where the time savings accumulate.

7. Real-Time Operational Risk Monitoring Replacing End-of-Day Manual Reviews

What end-of-day review cycles miss and why regulators are paying attention

An end-of-day operational risk review is a summary of what happened. By the time a team reviews it, the trading day is closed and the settlement window has passed. Any operational failure that occurred at 10 AM is discovered at 6 PM, after its downstream effects have already propagated. Regulators reviewing AI investment bank deployments are increasingly focused on whether risk monitoring is genuinely continuous or whether it is a real-time dashboard built on end-of-day data.

The distinction matters. Business process monitoring that updates every 24 hours does not provide early warning. It provides an audit trail.

Building a monitoring architecture that humans can actually act on

The most common failure mode in AI-driven risk monitoring is alert fatigue. A system configured to flag every deviation from baseline generates hundreds of alerts per day. Teams learn quickly to ignore low-severity alerts, and eventually stop engaging with the monitoring system altogether. This is a design problem, not an AI problem. Monitoring tools that do not prioritize alerts by severity, context, and required action time create noise rather than signal.

Effective real-time monitoring architecture assigns severity levels, routes alerts to the team with authority to act, and suppresses redundant notifications once an issue is acknowledged. The human oversight model is designed in from the start, not added as an afterthought. For an ai investment bank deploying this architecture, the outcome is a live operational health picture that teams actually use, rather than a dashboard that runs unattended.

Frequently Asked Questions

What does an AI investment bank actually do differently in back-office operations compared to a traditional bank?

An AI investment bank deploys agents that handle structured, rule-based back-office workflows end to end, including trade reconciliation, compliance monitoring, and regulatory reporting, without requiring manual handoffs between steps. The key difference is continuous operation and real-time exception handling. Traditional banks rely on batch processing and human review cycles that introduce delays and error accumulation.

Is artificial intelligence in investment banking replacing back-office jobs or changing them?

Artificial intelligence in investment banking is restructuring back-office roles rather than eliminating them outright. Repetitive data entry, manual matching, and document collection are being automated. Staff are shifting toward exception review, process oversight, and decision-making at defined checkpoints. The volume of purely manual tasks decreases. The requirement for judgment and oversight does not.

What are the biggest risks of artificial intelligence in banking back-office functions?

The main risks of artificial intelligence in back-office banking are alert fatigue from poorly designed monitoring systems, over-reliance on automation in regulated steps that still require human sign-off, and data quality problems in source systems that AI agents inherit rather than fix. Proper data management protocols and human oversight checkpoints address the majority of these risks before deployment.

How long does it take to implement AI workflow automation in an investment bank's back office?

Implementation timelines vary by function and existing system complexity. Single-function deployments like invoice automation can go live in weeks when source systems are accessible and workflows are documented. Multi-function deployments that span reconciliation, compliance, and reporting typically take several months for process mapping, integration, and testing before full operation.

Which back-office function delivers the fastest ROI when an investment bank deploys AI first?

Trade reconciliation and invoice processing consistently deliver measurable ROI earliest because both involve high transaction volumes, clear error costs, and well-defined process rules. The combination of volume and rule clarity means AI agents can take over the majority of the work quickly, and the cost reduction in manual labor is visible within the first operating quarter.

Conclusion

Most back-office teams in financial services face the same decision right now. Wait for enterprise software vendors to build AI into existing platforms, buy point solutions for individual functions, or implement an agent-based workflow platform that maps processes first. Each path has a real trade-off.

The first path is slow. Enterprise software development cycles do not move at the pace of your operational problems. The second path creates new fragmentation. Adding a reconciliation tool, a compliance monitoring tool, and an invoice automation tool separately rebuilds the same disconnected stack you are trying to escape. The third path requires process discipline upfront. You need documented workflows and clear ownership before automation begins. But it scales without adding headcount, and it handles the connections between functions rather than each function in isolation. The right path depends on two things: whether your core back-office workflows are documented, and whether your pain is concentrated in one function or spread across multiple handoffs. In the next 18 months, AI investment bank deployments will move further into cross-function orchestration, where agents manage not just individual tasks but the handoffs between them.

If your back-office workflows span multiple systems and manual handoffs, see how Predflow maps and automates complex financial processes end to end, without replacing your existing tools. Explore Predflow for Finance Teams.

FAQ

Frequently asked questions

What exactly is an AI agent

An AI agent is an autonomous system designed to handle specific business tasks end-to-end. Unlike simple chatbots, AI agents can reason, take actions, integrate with tools, and follow defined workflows.